The Constitutional Court

of the Republic of Indonesia

of the Republic of Indonesia

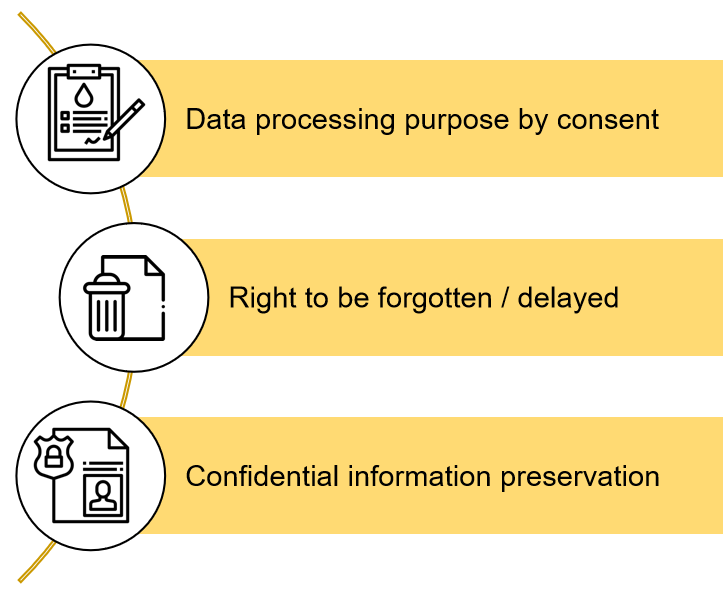

GenIO DataExchange, the foundational technology solution for compliance towards

Personal Data Protection Law No. 27 Year 2022.

Consent Management. Data Governance. Data Protection. And Data Retention.

More Info

GenIO

DataExchange

GenIO

DataExchange

The foundational technology for compliance towards

Personal Data Protection Law No. 27 Year 2022.

Consent Management. Data Governance. Data Protection. And Data Retention.

More Info

Join Us !

Looking for energetic people passionate about technology and building great businesses.

GenIO

Data Analytics & AI

Harness the power of your data for better decision-making, enter new initiatives and deliver better customer experience.

A complete big data lifecycle services from data collection and integration to data quality and data visualization & analysis.

GenIO

Master Data Management

Gain control of your data today! GenIO DataExchange to the rescue.

Improve data quality, create single version of truth of important data assets, and enable easier collaboration and shared data within your organization.

Medallion

Selling Agency and Wealth Management

Medallion Sales is a front to back selling agency and wealth management solution.

Transactional. Advisory. Self-service. All in one place.

Medallion

Custodian Services

Custodian consultancy, training and technology services.

Leverage on our expertise and modern technology to improve your custodian business.

GenIO

Regulatory Compliance

GenIO suite of regulatory solutions is Simian flagship compliance solution for banks and financial institutions providing an automated platform to meet their regulatory compliance needs.